Kirkland Didn't Buy Legal AI. They Bought a Moat.

On 4 June, Kirkland & Ellis, the highest-grossing law firm on earth, and Palantir announced an exclusive "Fund Formation Engine" for private-equity fundraising. It is the first shipped piece of Kirkland's roughly $500M AI program, built on Palantir's AIP and Ontology. It was unveiled at AIPCon 10, right next to Palantir's defense and industrial customers.

A founder friend emailed me the day it dropped, asking what I made of it. My honest first reply: lawyers aren't stupid about AI. But I couldn't figure out Palantir's play. Kirkland could pick any vendor for what they described, so why them? Fund documentation and side-letter drafting is not state-secret work.

I think I have the answer now. Kirkland didn't buy Legal AI. They bought a moat.

Sensitive

Before the moat makes sense, kill the assumption that fund formation is mundane paperwork. It is not state-secret work, I said that to my friend. But "not classified" is not the same as "not sensitive". Private-equity fundraising is some of the most commercially and relationally sensitive work in finance, and the shape of that sensitivity is exactly what rewards an ontology over a chatbot.

Start with the crown jewels: side letters and MFN clauses. Every limited partner negotiates bespoke terms, fee breaks, co-invest rights, excuse rights, a governance seat. A most-favored-nation clause then lets an LP claim any better term another LP got. So the moment "who got what" leaks, you don't get one awkward conversation. You get a cascade: every MFN holder reaches for the best terms in the room, and the fund's economics and its relationships blow up at once. The secret isn't the document. It's the map of who got what.

Around that sit LP identities and commitment sizes, fund economics (management fee, carry, hurdle), and track record and IRR. All confidential, and most of it regulated: the SEC Marketing Rule on how performance gets shown, Reg D on who can be solicited, AIFMD in Europe, KYC, AML and PII on the investors themselves. This is not "be careful with the file." This is "different rules for different fields, enforced."

Here's the part that decides the architecture. The sensitivity is fine-grained, not binary. Every LP must see a different slice of the fund, and none of them can ever see each other's. That is not a confidentiality problem, it's an entitlements problem: an access-control graph where each object carries its own permissions. A chatbot bolted onto a document pile cannot enforce that. An ontology with per-object permissions is built for exactly it.

Then the sting, which is also the honest tension hiding under "Palantir won't access client data." Aggregation makes everything worse. One side letter is sensitive. The terms and allocations of every fund, drawn from 1,000+ lawyers on $500B of client capital, form a live map of how the private-capital market prices itself. That is more sensitive than any single document, and a far juicier target. The same ontology that builds the moat concentrates the risk. Which is the whole point: this needs relationship-grade, per-entitlement confidentiality, and that is why the data model, not the model, is the thing Kirkland actually bought.

Moat

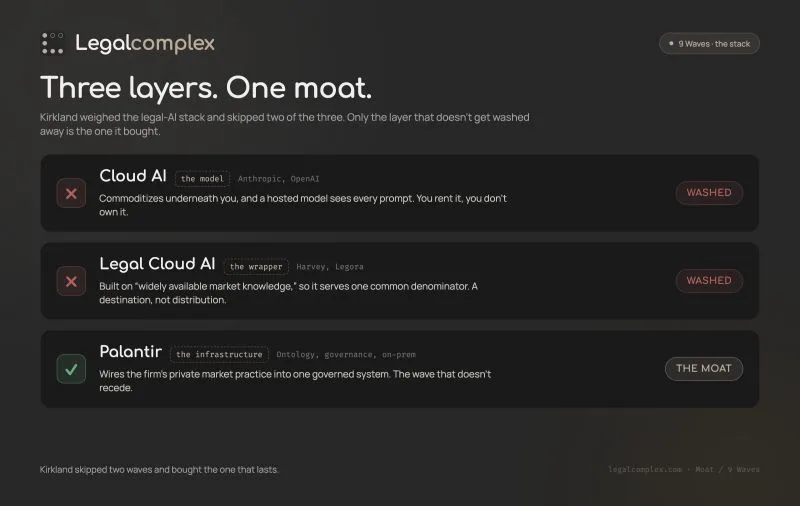

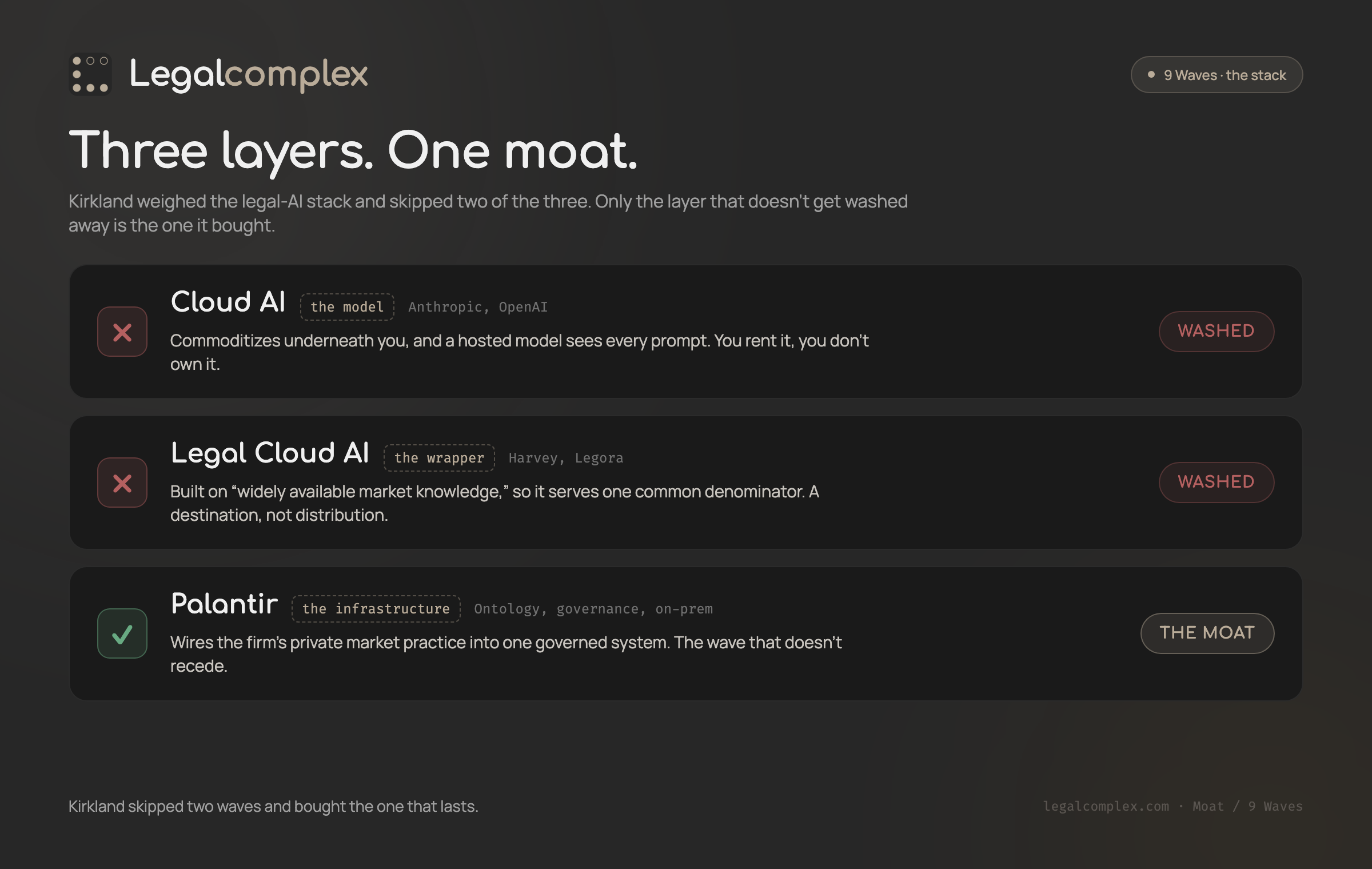

Last July I argued that legal data is no longer a moat: everyone has the cases, everyone has the statutes. The AI model is no moat either, clients switch the model underneath the way they switch a phone carrier. Two things still defend a position: private, personal legal data, and legal infrastructure (accurate, recent, consistent outputs, secure AI-to-AI plumbing, continuous compliance). Plus evals, the judgment that tells you the output is actually right.

Read Kirkland's engine against that list and it's a checklist, not a coincidence. The institutional knowledge of 1,000+ funds lawyers is the private data. Palantir's Ontology is the infrastructure that wires it into one operational system. Erica Berthou calls it a "revolutionary fund formation engine," a system that "centralizes and compounds the expertise of its most senior lawyers." That is just another way of saying the evals are proprietary. Kirkland built the moat exactly as drawn.

Washed

So why Palantir, and not Legora, Harvey, or any of the Legal AI names? And why not just rent a frontier model from Anthropic or OpenAI? That was my friend's real question, and mine. The answer is in a piece I wrote in November, the one where I argued the reign of OpenAI is over. Map legal AI as waves. The frontier model is one wave. The Legal AI wrapper sitting on top of that model is another. Both get washed away: the model commoditizes underneath you, and the wrapper is a destination, not distribution. Kirkland skipped both. Infrastructure is the wave that doesn't recede, and that is the layer it bought.

This is what the deal actually exposes about the Legal AI players. Palantir said it out loud in its own announcement: off-the-shelf tools are "trained on widely available market knowledge," so they "serve one common denominator." That is the flaw. A wrapper runs on the same public, common knowledge every competitor can buy. The real moat is the opposite of common. It is the legal matters Kirkland's lawyers have actually prepared, the judgment they bring to them, and the prior deal data that is the firm's own market practice. No vendor sells that, because it isn't for sale. It accumulates inside the firm, one fund and one side letter at a time.

And the market does its own gating. Fund formation for the big private-equity houses is high value and low volume: a narrow market, served by a short list of elite firms. There is no public corpus to learn it from, because the volume is thin and the terms never see daylight. Only the firms already doing the work hold the market-practice data, and doing more of the work is the only way to get more of it. The moat is gated by the very thing that is the moat, and Kirkland sits at the top of that list.

So Kirkland could pick any vendor for a model. There are dozens, and next year there will be dozens more, cheaper. What you cannot rent off a shelf is a governed, ontology-shaped, on-prem-capable layer that wires your own market practice into one system. Palantir isn't a wrapper, it's the connective tissue. That is the difference between renting a capability and owning a moat, and it is the entire reason the check went to Palantir.

Building this yourself is very, very hard. I said as much in August when Harvey tied up with Wolters Kluwer: even $9 trillion of Apple, Microsoft and Meta couldn't shortcut it. $500M and around 180 AI hires is the price of doing the hard, moat-worthy thing instead of renting a wrapper.

Signal

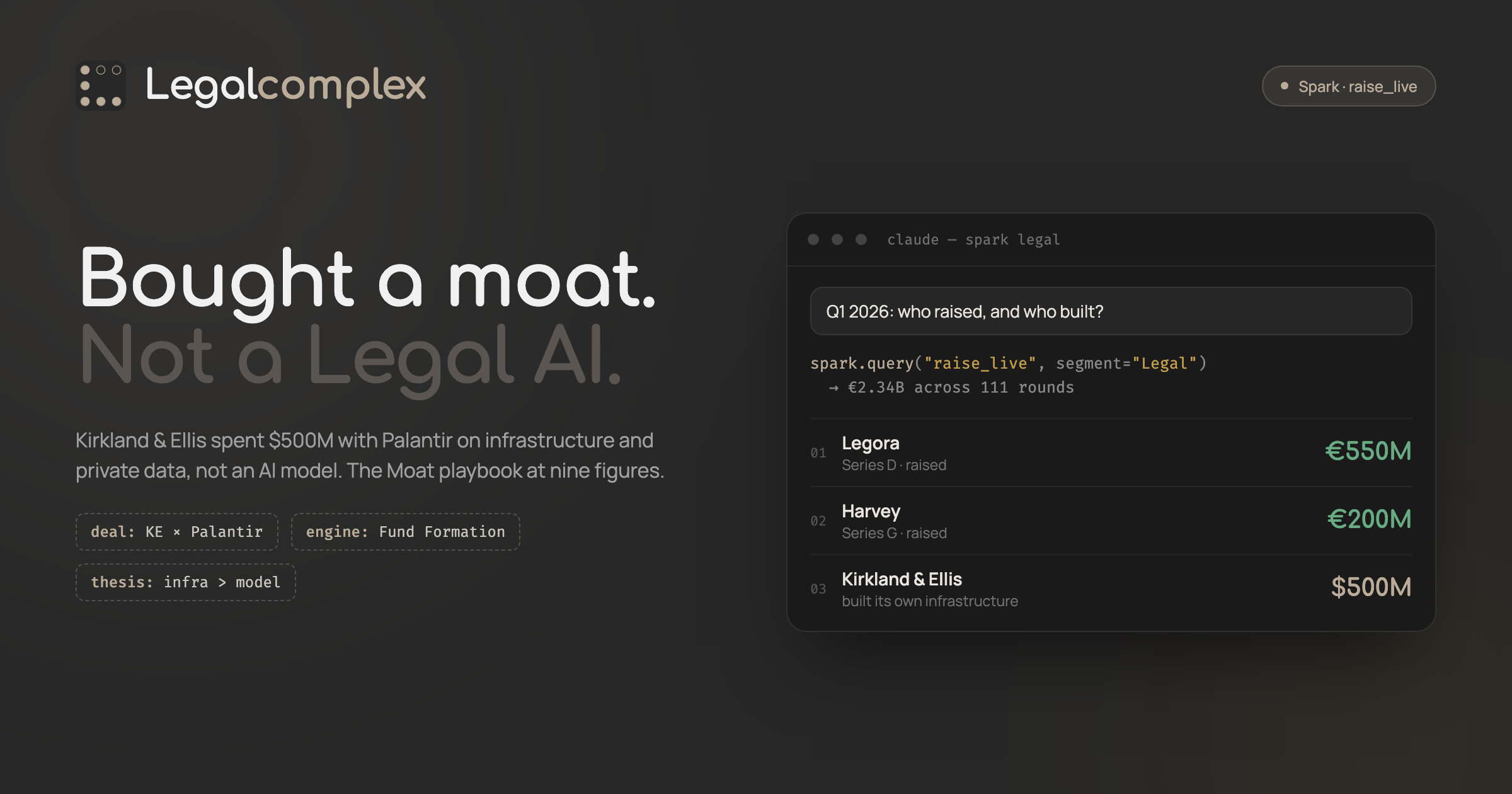

Zoom out, because the deal is a market tell. Spark, our own legal-tech dataset, has the legal segment pulling €2.34B across 111 rounds in Q1 2026, the strongest first quarter since the €3.42B AI-boom peak of Q1 2024. The money is there. Legora raised a €550M Series D and Harvey a €200M Series G inside two weeks of each other in March. Vendors are not short of capital.

So watch what the biggest buyer did with its money. Kirkland didn't write a check to a vendor and didn't buy one. It spent $500M building its own infrastructure. The same week, Kilpatrick stood up an in-house AI Lab and Ironclad's founder left to build legal products inside OpenAI. The top of the market is building, not buying.

Now look at where the bought vendors actually go. The legal M&A column this year is the wrapper layer folding into bigger things: Thomson Reuters took Noetica AI, Legora took Qura, Doctrine took Maite, Filevine took Pincites, LawVu took ClauseBase. That is the 9 Waves prediction on a spreadsheet. Capital floods the wrapper layer, then the wrapper layer gets rolled up. Infrastructure is the thing the players with the most to protect chose to own outright.

Appliance

There's a name for what this is. A walled garden. SmartEsq's Esther Chiang called it precisely that in the most-shared independent take on the deal, "The $500 Million Walled Garden". She's right about the shape, even where I'd push back on the verdict. A private system that runs AI on your data without handing that data to anyone else is the appliance thesis. Your AI like your office printer, in the building, not in someone's cloud. Kirkland's "Palantir won't access client data" plus its stated ambition to fine-tune open-source models on its own on-prem GPUs is that thesis at nine figures.

I'll say the quiet part once and move on: this is the bet Sabaio made, and we were about 16 months early. The market needed a $500M proof point to believe a private AI appliance was worth building. Now it has one.

Seam

Here is where I part company with the pure walled-garden story, because the walls are only ever as private as two seams nobody likes to mention.

The first is the primary-source seam. Real legal AI eventually needs the law, and people assume reaching for the law means leaking data. Mostly it doesn't. Statutes, regulations and case law are public record; Kirkland can pour the raw corpus into its own ontology and nothing confidential flows out. The leak isn't the law. It's the editorial layer on top of it, the Westlaw and Lexis headnotes, citators, the "is this still good law?" check, because querying that vendor can carry confidential context inside the question itself.

The second seam is bigger, and it's the model. A hosted frontier model, OpenAI, Anthropic, Google, sees every prompt, and in fund formation every prompt is dripping with LP names, commitments and side-letter terms. "Palantir won't access client data" governs the deployment. It says nothing about the model vendor. This is why Kirkland's on-prem GPU and fine-tune-open-source hiring is the load-bearing part of the whole program, not a footnote. Rent a hosted model and my own argument about confidential AI data, that it currently only runs under US or Chinese jurisdiction, applies to Kirkland verbatim.

So why does the moat hold? Because Kirkland chose the one practice area where both seams are narrowest. Fund formation is a closed world. The precedent is Kirkland's own, private by definition. And where it touches regulation, the public text is ingestible while the interpretation comes from those 1,000 lawyers. The institutional knowledge substitutes for the Lexis editorial layer. The moat replaces the vendor you would otherwise have to share with. That is not an accident, it is why fund formation is use case number one. The day this expands to litigation or open research, where validated vendor primary law is unavoidable, the seam reopens. On-prem open-source models are the only thing that closes it for good.

Buzzkill

Let me argue against myself, because a smart reader will. Three objections.

One: maybe there's no moat at all, just good repackaging. Strip the enterprise vocabulary and a lot of this is knowledge management and workflow automation with a Palantir logo on it, as Artificial Lawyer gently noted. Fair. Part of "why Palantir" is positioning, not physics. But positioning a competitor cannot buy is still a moat, and the ontology-plus-entitlements shape is real engineering, not a sticker. Some of the nine figures bought a story. Not all of it.

Two: if the edge is a walled garden, what stops Palantir building the next garden for the next firm? The exclusivity only covers this fund-formation iteration. Build enough of them and a private appliance stops being an edge and becomes table stakes. True. The moat is Kirkland's for now, the category is not defensible forever. First mover with the deepest private data wins the interim, which in this market is most of the game.

Three, the one aimed at me: of course the deal fits my frameworks, I wrote the frameworks. A hostile reader says I see moats and waves and appliances in everything because those are my words. Guilty enough to say it out loud. The test isn't whether the deal flatters my priors. It's whether the priors called the shot: pick infra over a model, minimize the seams, point it at the closed-world practice area first. It did. If it hadn't, I'd be writing a different post.

The moat reading holds. The durability doesn't. And the risk I can't argue away is the next one.

Independence

One risk left, and it's the one I've flagged for years. Legal professionals are allergic to monopolies and ethically required to be independent. A walled garden owned by a single mega-firm cuts straight against that. It is exactly what powers Chiang's conflict-of-interest critique: when a law firm becomes a software vendor, will rivals route their most sensitive deal flow through a competitor's platform? Allen & Overy and Freshfields are wrestling with versions of the same question. And a former judge, John Browning, has warned that the data-as-platform-property risk rhymes with the early cloud contracts. That is where the duty to safeguard a client's property and data got learned the hard way.

None of that sinks the deal. It sharpens it. Kirkland bought infrastructure and private data, the two durable moats, and packaged them as a private appliance. Then it pointed the whole thing at the one practice area where the data model does the defending and the seams stay narrow. That is a textbook moat. One question decides whether it's also a precedent for the rest of us: will a market that needs independence accept its best tools coming from inside its biggest player?

Lawyers aren't stupid about AI. Turns out they're not stupid about moats either.

Sources linked inline: Artificial Lawyer, Lawyer Monthly, the SmartEsq "Walled Garden" analysis, and my own LinkedIn work on moats, the 9 Waves, AI as an appliance, and legal AI data portability. Funding and M&A figures from Spark by Legalcomplex (legal segment, EUR). Framework archive at Raymond Blijd's profile.

Research base: 30 sources across 11 domains, 13 cited inline. Length: 2,315 words, a 12 minute read.