Q1 2026 Extended: Three Companies Took Two-Thirds of the Money

Legal tech raised $2.34B in Q1 2026. That is up 25.4% on Q1 2025, the second-highest first quarter on record after the 2024 AI boom, and a number that already made the earlier write-up on Artificial Lawyer. The headline is fine. The composition is the story.

One debt round changed the chart

Relativity took $720M in debt. That alone is 30.79% of every dollar raised in legal tech this quarter. Add Legora's $550M Series out of Stockholm (23.52%) and Harvey's $200M (8.55%) and you have three companies accounting for 62.86% of all Q1 funding. The remaining 97 companies split the other $872M.

The total is up. The breadth is not. 100 companies raised in Q1 2026, down 1% YoY. Deal count is 103, down 7.2%. The median round size collapsed to $1.0M, a 57.5% drop. That gap between a rising total and a falling median is the single most important signal in this quarter, and it is the same signal we have been calling out since 2024: the market is bifurcating. Mega-rounds at the top, seed compression at the bottom, very little in the middle.

Investors are still here, and that matters

Investor count was the surprise. 204 unique investors participated in Q1, up 36.9% YoY. More investors writing smaller checks into fewer companies is not a contraction. It is a sorting. Capital is still arriving; it is just being more selective about which doors it walks through.

The top 10, in full

| Company | Round | Area | City | Lifetime raised |

|---|---|---|---|---|

| Relativity | $720M Debt | eDiscovery | Chicago | $845M |

| Legora | $550M Series | Text Analytics | Stockholm | $816M |

| Harvey | $200M Series | Text Analytics | San Francisco | $1.23B |

| Fieldguide | $75M Series | GRC | San Francisco | $125M |

| Factify | $63M Seed | Contracts | Tel Aviv | $73.3M |

| Lawhive | $60M Series | Automation | Hyderabad | $114.2M |

| Crosby | $60M Series | Practice Mgmt | New York | $85.8M |

| Orbital Witness | $60M Series | Real Estate | Oxford | $75.0M |

| Ivo | $55M Series | Contracts | San Francisco | $77.2M |

| Summize | $54.67M Series | Contracts | Manchester | $59.7M |

Three observations from that list. First, four of the top ten are contracts companies (Factify, Ivo, Summize, plus Lawhive on the consumer end). Contracts remains the deepest-funded category in legal tech and is showing no signs of consolidation. Second, Factify raising a $63M seed is its own story: that is not a seed round in any normal sense of the word. Third, Hyderabad and Oxford in the top 10 alongside the usual SF, NYC and Stockholm names is a pattern we did not see in 2023. Geography is broadening even as company count narrows.

Geography: still North America, still concentrated by city

North America took $1.38B across 51 companies. Europe took $748.86M across 25, with Stockholm doing roughly all of the heavy lifting on the back of Legora. Asia raised $183.23M across 13. Africa logged 4 companies raising a combined $158.5K, statistically nil but the first time the continent shows up across multiple legal tech deals in a single quarter.

The city split is more telling than the continent split. Chicago at 30.8% is entirely Relativity. Stockholm at 23.5% is entirely Legora. San Francisco at 15.1% is Harvey, Fieldguide and Ivo. Three cities, three large rounds, more than two-thirds of the quarter. New York at 5.5% and Tel Aviv at 2.7% round it out. "Others" combined for 22.4% across the rest of the world.

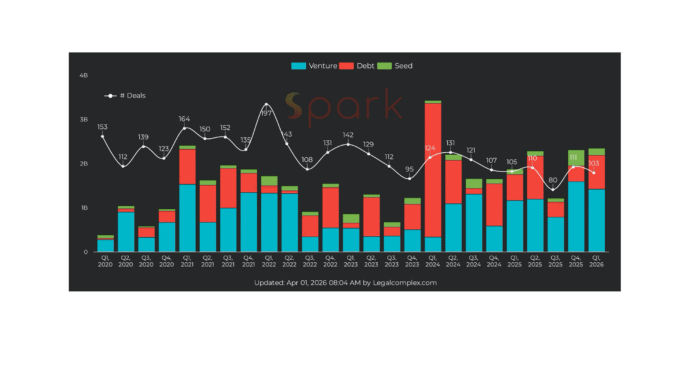

Q1 in historical context

Six years of Q1 data: $2.40B (2021), $1.71B (2022), $851M (2023), $3.42B (2024), $1.87B (2025), $2.34B (2026). The 2024 spike was the AI boom hitting at full throttle. The 2025 dip was the post-boom hangover. 2026 looks like the new normal: roughly $2B to $2.5B per quarter, give or take one mega-round.

Stripping the quarter into its components: $1.41B Venture, $765M Debt, $163M Seed. The 32.7% debt slice is the highest quarterly debt percentage we have on record outside of one-off facilities in 2024. That is something to watch.

Exits jumped, and that is new

Q1 2026 saw 32 exits. Q4 2025 had 14. That is a 128% quarter-on-quarter jump in exit activity, off a low base, but the trajectory matters. Funding deal count has been bouncing around 100 to 110 per quarter for over a year, suggesting a stable plateau. The exit line spent most of 2024 and 2025 below 30. If 32 holds or grows in Q2, we are looking at a real liquidity cycle starting to turn.

That is a very different market from the one we wrote about a year ago.

Growth vs Seed: the crossover holds

The long-view chart is unchanged from the last few quarters. Seed deals (59) continue to outpace Growth deals (44) in Q1 2026. The crossover that started in Q4 2023 / Q1 2024 has now held for nine straight quarters. AI-native legal tech startups are still being born faster than the existing growth-stage cohort is graduating to Series B and beyond.

This is the structural story underneath all the headline numbers: legal tech is in a sustained generational reset. The companies funded heavily in 2021-2022 have either broken out (Harvey, Legora, Relativity) or are quietly being lapped by AI-native challengers raising $1M to $5M seeds.

What to watch in Q2

A few things will tell us whether Q1 was a turn or a blip:

- Does Relativity's debt round stay an outlier, or do we see more debt facilities for mature legal tech? Debt as a percentage of total funding (32.7% this quarter) is not normal.

- Does the exit count hold above 25? If yes, M&A is back. If it falls to single digits again, Q1 was acquirers cleaning out their pipelines after a slow 2025.

- Does the median round size recover? $1.0M is a stress signal. Either it climbs back toward $5M (healthy market), or seed compression continues and the bifurcation gets worse.

- Where do the next mega-rounds go geographically? Stockholm and Oxford on the same top-10 list was a 2026 first.

The Spark dashboard updates daily. The full data, including the per-deal table and the geographic breakdown, is at legalcomplex.com/research for paid subscribers, and the public Q1 summary lives on the earlier Artificial Lawyer piece.

Q2 starts now. We will see what the next 90 days say.

— RB

Data: Spark by Legalcomplex, all_live snapshot as of 2026-04-01. Segment filter: Legal. Excludes compliance-only and GRC-tangential companies unless legal practice is the primary use case.