Can Legal AI (Ever) IPO?

Well, it depends. Let's lay out the conditions needed to pave a realistic path to actually printing money. Previously, I stated that most top legal tech companies cannot IPO. Market conditions have not improved since. Nevertheless, any crisis offers entrepreneurs opportunities to capitalize.

IPO Prologue

Your AI or accountant will provide you with specific metrics to hit in preparation for an IPO. What I offer is a guide to the legal market reality that may enable you to hit those targets. Some numbers in Legal & GRC:

-

16,332 companies* in Legal & GRC

-

$342.90 billion in total raised to compete in Legal & GRC

-

$17.73 billion raised by 438 companies in 2026 alone (5% Seed, 31% Debt & 63% Venture)

-

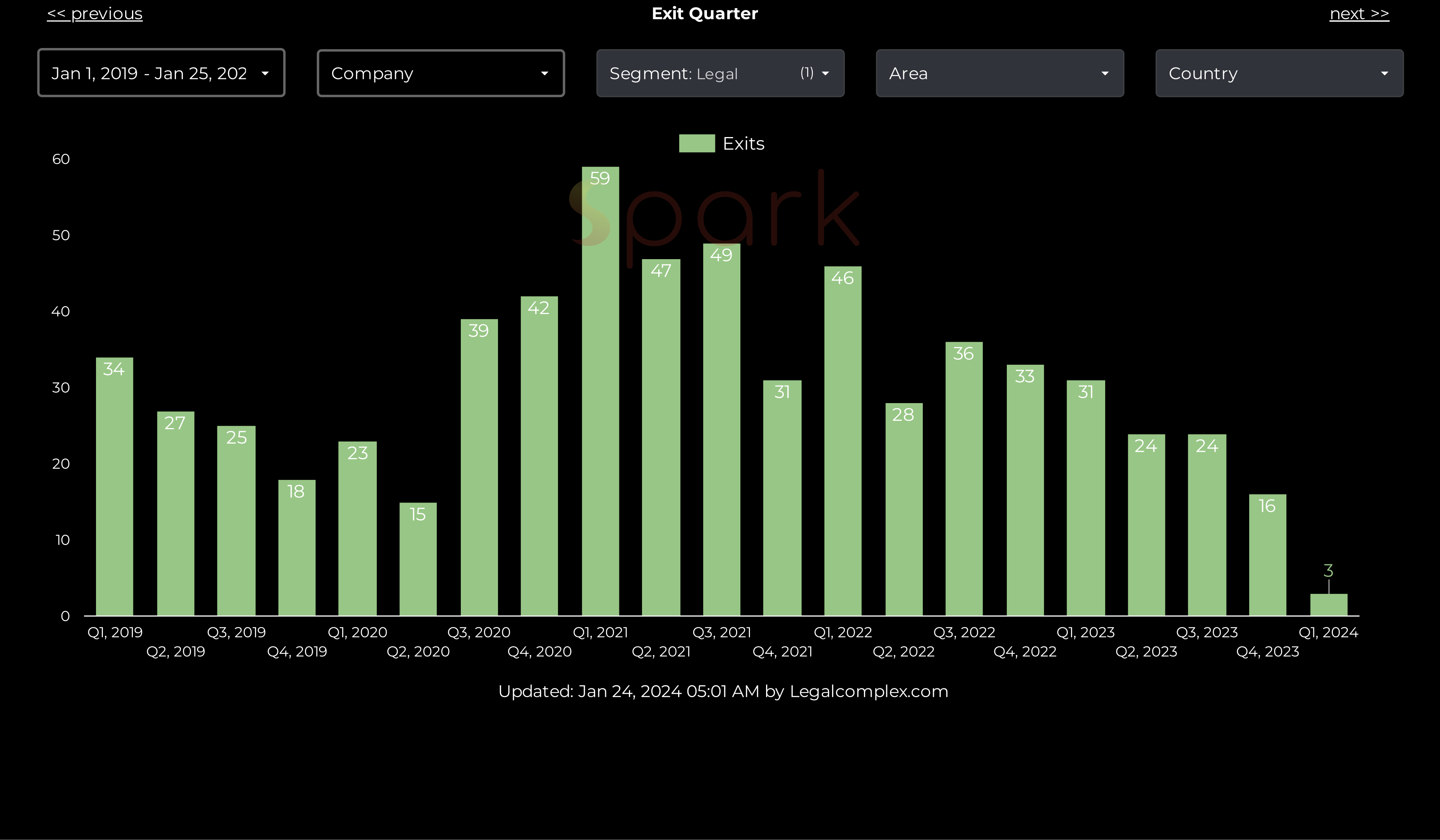

63 mergers and acquisitions tracked in 2026 with only 3 disclosed exit values (2 in Legal + 1 GRC)

-

$600 million in total exit value for all 3 exits above

-

0 (Zero) companies completed an Initial Public Offering (IPO) since 2021.

For context: 3 disclosed‑value exits out of 16,332 companies implies a 0.018% chance that investors see a successful return on their investment. That is 1 in 5,400 companies.

*Note that 16,332 companies do not include vibe-coded solutions. Welcome back to my world.

Why Most Legal Tech Never Cash Out

You're still here? Ok, optimist, there is a way to get paid.

The reasons a legal tech venture goes from startup to successful exit are laid out in Anatomy of a Legal Acquisition. TL;DR: the most upside is gained by not raising a lot. In a post on Artificial Lawyer, I shared data comparing valuations vs exit value numbers. Why not raise a lot or, even better, bootstrap? Because that makes you and your company affordable. Once a company has "borrowed" over a certain amount, options for a lucrative payday begin to evaporate. The only recourse is to offer your company to the public through an initial public offering (IPO). I would not bet on support from Private Equity (PE). Just ask Relativity. Also, remember when Docusign tried to go private? Going through a Special Purpose Acquisition Company (SPAC) is no guarantee either. SPACed companies like FiscalNote have not given me much hope based on their stock price history.

Surely there have been successful legal tech IPOs? Nope, not really. In 2023 we analyzed 17 public legal tech companies and, with the exception of the big three, all did poorly. Currently, Wolters Kluwer, RELX and, Thomson Reuters have lost more than half their value, with no signs of recovering it. Worse, their decline started at a very peculiar point, way before the infamous Anthropic Legal plugin dropped. Now these unprecedented low public valuations sit in stark contrast to late‑stage private legal tech valuations.

Fine, so this would not stop current legal AI companies from seeking an IPO, right? Relativity, a eDiscovery company, filed confidentially for its IPO on March 19. It would be the first legal tech company to go public since 2021. SpaceX filed 13 days later and is already trading. Relativity is not. Relativity still has no public prospectus, no price, no ticker.

Recap: If you are not cheap enough to be acquired, your plans to cash out reduce to zero. Unless you look like Palantir.

Why Most Legal AI Goes To Zero

As demand for AI compute grows, it has also drained the capital supply needed to fund that growth. Except for Apple, the rest of the "Magnificent Seven" are borrowing because they have no more free cash left to spend. The growth in demand for AI compute correlates with widespread use of AI. While AI use is popular with most, only a few sectors can afford to pay. The sector that has a lot of cash to spend seems to be law firms. And, boy, are they spending on legal AI if we believe the ARR announcements. Unfortunately, not everyone is so lucky and there are reports of layoffs by legal AI vendors. In other words, both legal AI budgets and AI compute spending are hitting limits.

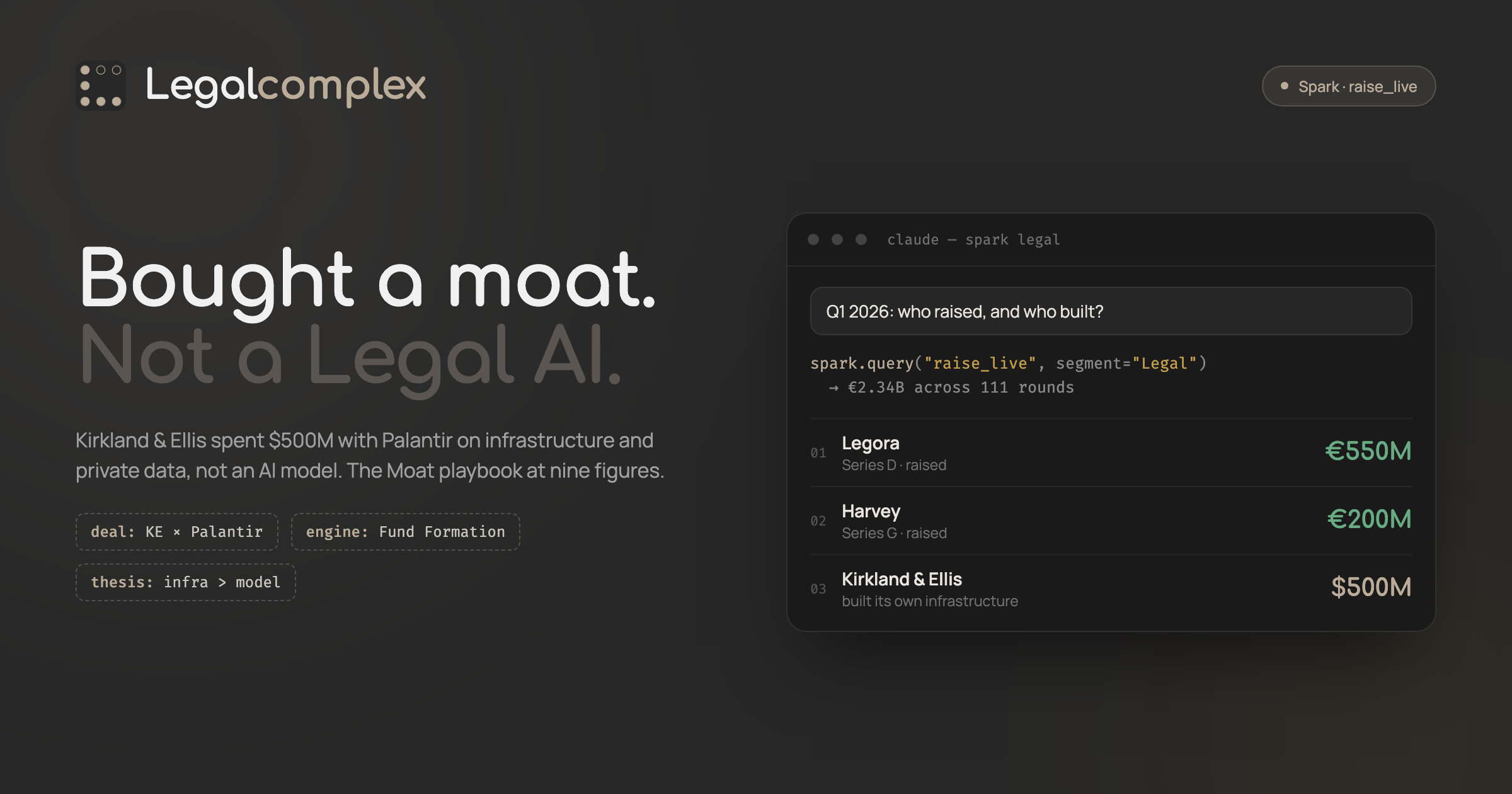

For argument's sake, let's say supply of AI stays abundant, as it currently still is. Where is the scarcity? Well, accuracy and security are still in short supply in the use of AI. That is why Palantir saw a record-breaking 85% revenue surge. Better yet, they are arguably the only profitable software company selling AI. Since they are a public company, we can verify their reported numbers. Wonder why profitable? Palantir sells on-premise AI (security) and an ontology (accuracy). Hence, I unretired from writing these analyses to explain Kirkland & Ellis's $500 million bet using Palantir tech.

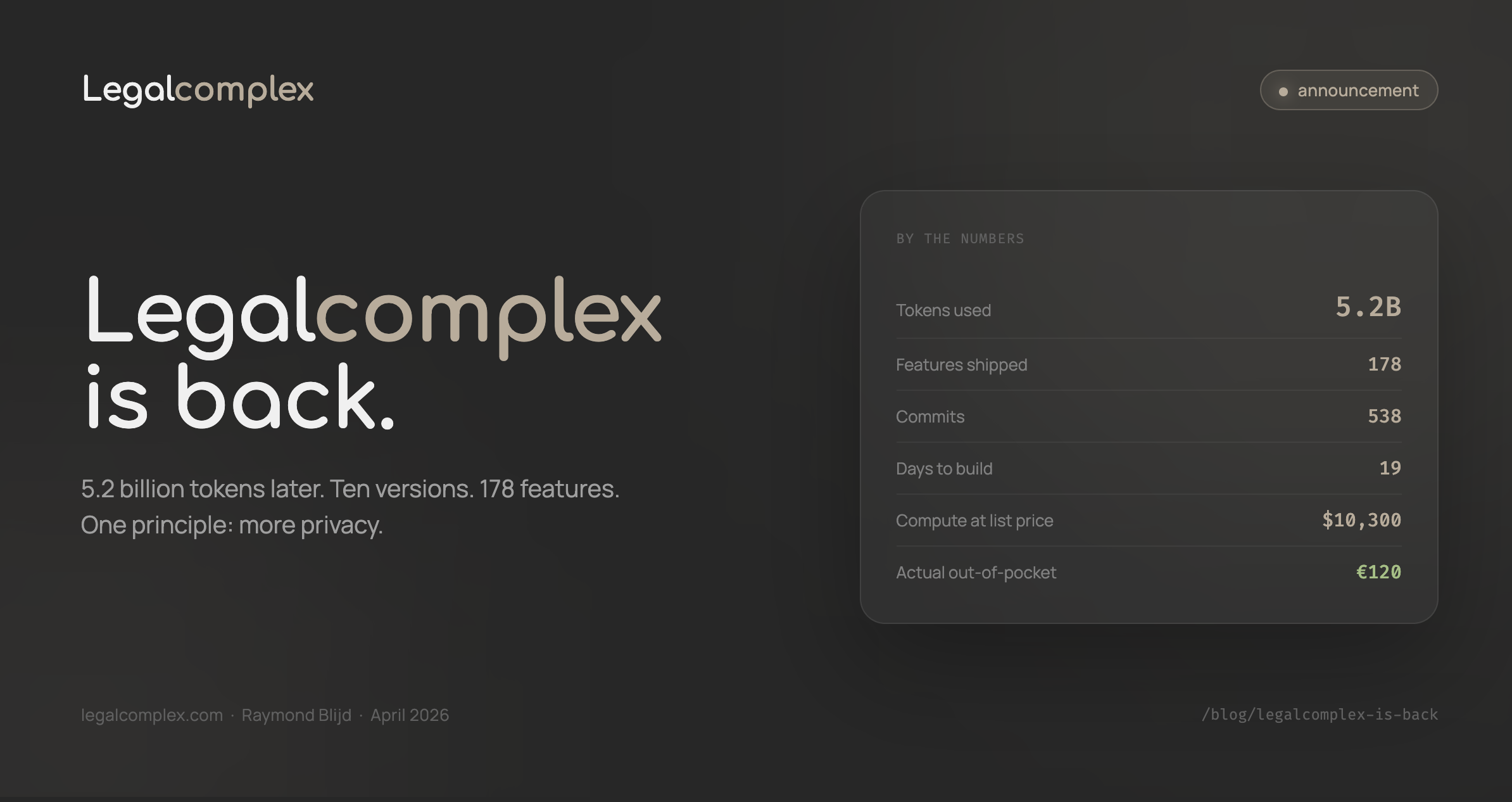

Another thing in short supply is affordable AI. I just rebuilt Legalcomplex on roughly 5 billion tokens. But the kicker is that I only paid €120 for total token use, which would otherwise cost around $10,300. That is why no one is making a profit except Palantir. Because everyone's AI use is subsidized, especially frontier AI use. So there is demand for accurate, affordable AI and autonomy. No one is able to supply it, and if they claim they can, they are lying. Lying because the constraints are physical, not digital: chips, electricity, water, and real estate.

Point: accurate, affordable AI that offers you autonomy is in short supply; everything else will likely go to zero due to abundance.

One Path To IPO

Obviously, only hardware companies offering physical solutions for AI are capitalizing. Software companies that support accurate, affordable AI and autonomy have a slim shot at profiting like Palantir. Examples are suppliers of unique data like Reddit user-generated answers. As a matter of fact, the only billionaires being created by the AI boom so far supply human‑verified AI data. While human‑verified data is proprietary, not all proprietary data is valuable. The data that is not valuable is government-produced legal data like legislation and case law. Although legal data is protected by copyright, governments are legally obligated to provide citizens with access to the law. This is contrary to privately produced legal data, such as Kirkland & Ellis.

The problem with privately produced legal data is that it is niche and thus only valuable under specific conditions. The same goes for automating legal processes. The key to identifying valuable opportunities is distinguishing volume from value. The acquisition of Twitter constitutes a high-value, low-volume legal process, as do fundraising and major corporate litigation. Given these high stakes, those processes remain human-bound despite being highly automatable. Not because humans are more accurate, far from it. It's because they are accountable. Last year, I gave a presentation in Madrid arguing that firms will be the ultimate winners in legal AI for one simple reason: accountability.

Although nearly all legal processes lend themselves to AI processing, only a subset requires human verification. Identifying this distinction demands the skill to determine which processes hold value. Legal practitioners may claim human involvement is essential in all legal processes, yet judicial recognition of e-discovery indicates otherwise. Despite this major legal victory, it has not translated into business wins for legal tech vendors. As I said: no successful public legal tech companies yet. Maybe Relativity? Smirk.

Path: Automating valuable legal processes may appear lucrative, but in reality it is not. The opportunity lies in making legal processes accountable by underpinning them with human‑verified decisions and data.

To All Legal Tech Companies

If you’ve raised $100 million or less, think hard before raising again. You might still have an acquisition, PE or SPAC exit option available. If you are above $100 million then shoving your shares onto the public may be your only option. In that case, you need growth, crazy growth. There are 336 companies that raised over $100 million (101 in Legal and 235 in GRC).

I am not saying lucrative legal tech exits are impossible. I am saying if your cap table requires IPO-level, there is one plausible path. You need to latch on to legal processes with value-to-volume ratios that make sense. Find a balance between high-value and high-volume legal processes with few competitors. Once you find high value processes, go look for a high volume of customers that are willing and able to spend.

Exit Epilogue

I used to write every month but stopped for one reason: AI. Now AI actually made me want to write again. To organize my thoughts and rationalize my reasons in my own written words. Not AI-generated.

Sources linked inline. Legal-tech funding and M&A numbers from Spark by Legalcomplex. Figures dated to mid-2026.